Universal access to electricity has been on the rise since the early 2000s, particularly across key low income countries (India, Myanmar and Kenya to name a few), where energy access policies along sustained investment initiatives have helped accelerate progress and promote access to modern energy as a key priority. There are some encouraging signs that energy is becoming more sustainable, more affordable and increasingly widely accessible.

Putting this into context, in early 2000s circa 73% of the Global population (24% of sub-Saharan Africa) had access to electricity; in 2018, this number jumped up to over 89%. That equates to an estimated 2.2 billion people. An eye opener and significant milestone that delivers to the most in need. Nonetheless, today nearly 860 million people, all in low income countries, continue to live without electricity. Moreover, 80% of which reside in sub-Saharan Africa.

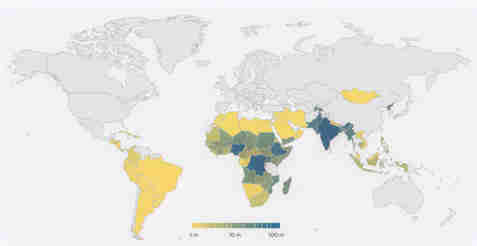

Population with no access to electricity

The global demand for power in emerging markets is only growing, now expected to double by 2040. In the face of rapid population growth, without more sustained and emboldened actions, by 2030 over 650 million people will continue to lack access to power. A number, very hard to digest, equal to the population of all the European Union, Brazil, Mexico and Turkey combined!

In summary, universal access to power is a task far from completed. Contrary to some who claim victory on achieving SDG 7, the reality is the goal is still far from reached. The challenge ahead of us would require tripling the average number of people gaining access every year from around 20 million today to over 60 million people. An ecosystem of new and scalable energy solutions is needed for rural and semi-rural communities. Today we are not there yet.

Number of people without access to electricity in sub-Saharan Africa (IEA)

Off-grid Solar Lighting: A Solution to the Grid?

Since the early 2000s, off-grid solar has been an evolving solution to address the energy deficit in emerging markets. Today the knowledge gap about effective off-grid technologies is largely bridged; the solution is more feasible and it is becoming increasingly commoditised as equipment prices (and minimum scale) continue to reduce. Today we know that off-grid solar can be an effective (and lucrative) solution, granting access to electricity to millions in need.

In parallel, integrated utilities continue to face significant challenges, a decentralised off-grid sector is advancing rapidly beyond simple lighting and phone charging, early movers in the market now need to evolve their business models in order to realistically confront their own financial impediments. As Kleos Advisory report indicates, “The combination of solar and fintech is driving an economic transformation, making the ‘unbankable’ bankable and embedding African consumers in the digital economy.”

All companies, whether early, established entrants (Gen-1) and recent challengers (Gen-2), have yet to overcome evident financial challenges that arise when scaling up the different pay-as-you-go (PayG) models – differing by system capacity demand:

-

Pico PV / Solar Home Systems (SHS): focused on off-grid households with power needs of up to 250Wdc (direct current)

-

Nano-Grids, mesh-grids, solar containers, kiosks, and DC mini-grids: solutions ranging from SHS to more centralized community or village solution with power needs of up to 500 kWdc

-

Mini-grids and rural utilities / DESCOs: Remote grids for new residential & small commercial customers with power needs up to 5 MWdc.

The attractive market opportunity often distracts readers from the growing market dislocation, regulatory hurdles and especially financial challenges. For instance, despite first mover advantages, instrumental with the creation of a vibrant off-grid market, Gen-1 companies are now fighting for survival. Initially promising business models, usually integrated, are burdened with high working capital needs and demand constant access to financing (e.g. PayG model which allows customers to purchase their off-grid energy systems over time are prone to delinquencies which if not well monitored required exacerbate capital requirements). In markets where access to alternative capital tends to be limited, this continues to be a bottleneck for growth.

Access to financing is a common problem, as industry executives point out: “the biggest pain point is access to capital especially for companies that are not among the cohort of start-ups that commenced operations 1012 years ago”. The arrival of off-grid solar in the last decade was new whose challenges were not fully understood. We must rise to the occasion to overcome those challenges to avoid falling short of delivering credible and sustainable results.

Off-grid Solar: Investment Flows Dynamics

Early start-ups that have become mature businesses, have grown in a sector given their first mover advantage to capital and customers. According to Wood Mackenzie, approximately US$ 2.1 billion in cumulative disclosed corporate-level investment was deployed into off-grid energy access markets between 2010 and 2019.

For instance, PayG models attracted more than US$ 600 million in funding so far from institutional, impact and reputable strategic investors including utilities such as Engie, EDF, EDP and Total. The investor community embraced the initial hype, aiding quickly fast-growing stories and delivering on many of the KPIs sought, but with “unproven” business models and questionable paths to profitability. While capital flowed into the sector, some impact investors, developing financial institutions, foundations, multinational development banks (“MDBs”) and strategic investors became increasingly wary of their investments. As many off-grid companies started to mature, financial challenges have become evident. Recently, as the solar business has become even more commoditised, circa 80% of Gen-1 players – many which continue to be funded — fail to deliver on financially sustainable business plans.

Funding concentration has largely been another big issue in the last decade showing no sign of improvement. Circa 90% of all debt and equity investments continue to flow to the largest ten players. What’s more, over 78% of any equity, debt or grant financing is actually going to largest three players. Africa specific, as witnessed in GOGLA’s 2020 Off-Grid Solar Investment Report, finds that over 75% of all commitments in 2020 went to just three companies. Such concentration of funding reinforces the case that the industry is failing to support the ever-growing SME sector capital requirements for this huge, high-growth market.

Gen-2 players who have followed early entrants courageously and addressing the current sector challenges at scale, get a tiny apportion of financial support – this despite proving to be able to increase market share in the short term while incumbents remain tied to older technology purchase contracts. Relative competition amongst both Gen-1 and Gen-2 players drives business model innovation and better product offerings. Investment should now flow to newcomers.

Why are We far Away from Meeting SDG 7?

The overall financing requirement to meet SDG 7 is estimated at US$ 1.3 trillion per year until 2030.

Slow development and scaling of off-grid power in low income countries can be traced to its lack of funding, which today consists mostly of donor grants, debt from international development finance institutions (DFIs), investment from private institutions and, owner’s equity, bearing the highest risk. So why are investors crowding in this space?

While the renewable energy from off-grid infrastructure is relatively low cost, users in need of such products have meagre savings and limited financial capacity and therefore, can struggle to afford electricity. Others who can afford the solutions on a cash basis struggle to afford the upfront costs, as well as monthly cost of energy from a national electrical grid connection may also be out of reach for many.

In most cases financing to rural households with limited finances for SHS remains unaddressed. Commercial banks and micro-finance institutions tend to not extend credit for SHS and mini-grid utilities, citing risks. DFIs have not lived up to expectations and failed in mobilising private sector financing at scale, mostly supporting a subset of operators craving for low-cost debt.

A joint approach is needed for those seeking to perform a catalytic, additional and in turn riskier role to mobilise private capital. Development agencies, philanthropic foundations and government-backed institutions should not be afraid to take risks in an effort to mobilise the private sector. Using development capital to create risk-return profiles acceptable for the private sector has proven to be a practical approach crowding-in institutional capital towards SMEs. Without it, funding will not reach segments with the highest unmet financing needs, such as small- and medium-sized enterprises.

Does One Solution Fit All?

Sub-Saharan Africa has +600 million people without access to electricity and even those that have some connection to a local grid suffer with poor service reliability. In rural areas, where population is less dense, it has been expensive and difficult to provide grid access. At the current trajectory, population growth is set to outpace new connections before 2040, such that 95% of the remaining global unelectrified population will be in sub-Saharan Africa.

Electrifying Africa is one of the largest development challenges today. Until recently, most people assumed that the continent would electrify in the same manner as the rest of the globe. Given the challenges with commissioning new utility grid power, coupled with improving and expanding electrical transmission with current financial status of most regional utilities, sadly sub-Saharan Africa will take decades to fully develop.

The arrival of off-grid solar power in Africa in the mid-2000s was heralded with much fanfare. Unfortunately, we are seeing just how much of a challenge in delivering power that has been. Solar power only represents 1% of total capacity installed in Africa, and off-grid is only a portion of it. Currently, just 3% of the continent’s population has access to off-grid solar systems. This is an improvement and a step in the right direction, but not the miracle solution we may have been led to believe in.

The bankability of these solutions is the main issue. Solar lanterns and solar home systems are an effective solution for the unbanked rural households; however, small-scale solutions cannot power growth and industrialisation. Timid commitments to justify alignment to specific KPIs won’t solve the problem.

The arrival of Covid-19 marked a new challenge for all companies in the renewable energy sector ecosystems. We see how investments in the sector are often limited by investors’ myopia with what works and what does not. The emergence of Gen-2 players, as well as newly formed downstream partnerships, are delivering faster, better and more agile solutions to the energy challenges on the continent. We shouldn’t squander resources in supporting entrepreneurs who are truly committed to overcome challenges.

Covid-19: “Houston, We Have a Problem”

According to research published by ENDEV, almost 9 out of 10 players in the off-grid space across low income countries will be struggling for survival in the next 5 months. Industry sales volumes are down, smaller players lacking access to capital, with a number of other factors hampering activities. Most of the companies have been unable to access financial relief, particularly those who were not initially invested by DFIs and multilateral institutions (currently prioritising portfolio companies).

Smaller power producers and distributors are more affected during this period and are struggling to stay afloat. It is very evident that the mobilisation of different capital sources is key to reach the solutions needed faster. The COVID pandemic has drawn attention to the need, now more than ever, to make grant instruments available in addition to concessional loans. Noise on credit to the unbanked is an issue, echoing the noise on the need for an MDB-led Pan-African off-grid guarantee programme – focused precisely on de-risking where is needed the most.

With enhanced capacity building to qualify solar technicians, availability of vast financing mechanisms, and continued support to streamline policy and regulatory frameworks, off-grid solutions have a real potential to fill the missing middle. However, unless further action is taken, many more players are on track to joining the Mobisol and SolarKiosk list.

The Need for Public Means for Private Sector to do More

The private sector is crucial for the future development of bigger projects, as explained by Winrock International in their publication to the World Bank: “with the right set of regulatory and financial incentives in place, investors will flock to the continent and inject the capital and the knowledge necessary to foster a viable middle class”.

Lessons have been learnt on “reaching critical mass” may not be the value-enabler initially envisaged in academic research, the importance of the book & customer quality is more critical and beyond hitting the “acceptable” numbers. Public financing must find ways to coherently support the rural electrification transition to bring confidence to mainstream financial markets. New research from British think tank the Overseas Development Institute, finds that the MDBs are failing to meet expectations when it comes to catalyzing additional private finance into low-income countries, mobilizing just US$ 0.37 of additional capital for every US$ 1 of public money invested. Further, according to The Center for Global Development, private flows were falling instead of rising and that despite their potential to act as catalysts, MDBs had only played a “marginal role.” Significant change is needed to the MDB’s financial models, and greater collaboration with the private sector and alternative asset managers.

Now that the market better understands the technology, the risks, and that the costs have been driven down over the years, perhaps we will see increased MDB support as a credible alternative to the funding deficit to the sector. With the Covid crisis impacting economies, sector focused-SMEs will require funding, or off-grid will be set back even further.

Annual Investment Shortfall in Emerging Markets to meet SDGs by 2030

What’s the Outlook?

For a long time, we trusted that organizations such as the World Bank, NGOs and the UN would solve these problems. Unfortunately, this is not happening – or not at the pace we expected.

It is very evident that the mobilisation of different capital sources, primarily the private sector, is key in getting closer to mobilising the additional capital required. Matching the various risk appetites, or traditionally “blending” is an approach that has proven to be effective. This concept would serve the off-grid financing markets very well and might be the way to embolden and accelerate the much-needed action. But the implementation has to go beyond just the few well-funded companies in order to prove we are collectively committed and entrust others to join in this cause where needs everyone to play a role.

Overcoming the challenge is needed to ensure the correct target groups are the ones who benefit. As a recently published ODI reports finds “Instead of going as planned to low-income countries, most concessional finance being provided to blend with private money is going to middle-income countries”.

The off-grid energy market holds a more promise beyond lighting unlit households and reducing the cost of power, it is understanding energy as the medium for financial inclusion: “Basic goods might not be what matters above all else, but they nonetheless matter a great deal”. (Reiner, 2018).

Themes we hope to see shaping in the next year:

-

Steady realignment on international development-focused agenda i.e. a push to mobilising private capital through public sources (that is developmental institutions leading – and taking higher risks – than private investors).

-

Acceleration on cross-sector downstream partnerships, seeking to providing human capital resources and support, branding, and networks – mobility, power and financial inclusion as the true service (and value) proposition.

-

Funding concentration is an indicator of market dislocation – and not the best way for a decentralised sector to prosper. Public bodies should lead the way in recognising this is critical in creating capacity beyond the few “SMEs” – and must – support businesses outside their existing “portfolios”.

-

Dedicated top down policies to encourage north south investment – for example, through the UK, Japan-focused mission is helping to drive development in the sector by combining different essential attributes and resources, with new partnerships emerging (Azuri/Marubeni and BBOXX/Mitsubishi)

-

Local and international alternative investors supporting an acceleration in balance sheet financing receivables for SHS portfolio companies & selective capital migration to bankable-offtake models e.g. semi-rural, C&I.

-

Unbundling PAYG solutions. While counterintuitive, on-grid sector, necessary for industrialisation and economic growth will also require integrated electrification planning as demand shifts to off-grid solutions

Links

1) Schneider Electric – https://download.schneider-electric.com/files?p_enDocType=White+Paper&p_File_Name=998-2095-07-28-15BR0_EN.pdf&p_Doc_Ref=998-2095-07-28-15BR0_EN

2) EnDev – https://endev.info/content/COVID-19:_Energy_Access_Industry_Barometer

3) Energy 4 Impact – https://www.energy4impact.org/file/2086/download?token=9-hw5RF1

4) World Bank – https://data.worldbank.org/indicator/EG.ELC.ACCS.ZS

5) IEA – https://www.iea.org/reports/africa-energy-outlook-2019

6) Kleos Advisory – https://www.azuri-group.com/wp-content/uploads/2020/01/The_grid_wont_connect_Africa_but_solar_can_Kleos_Advisory_Report_1_2020.pd

7) No small hope – Towards the Universal Provision of Basic Goods, Kenneth A. Reinert